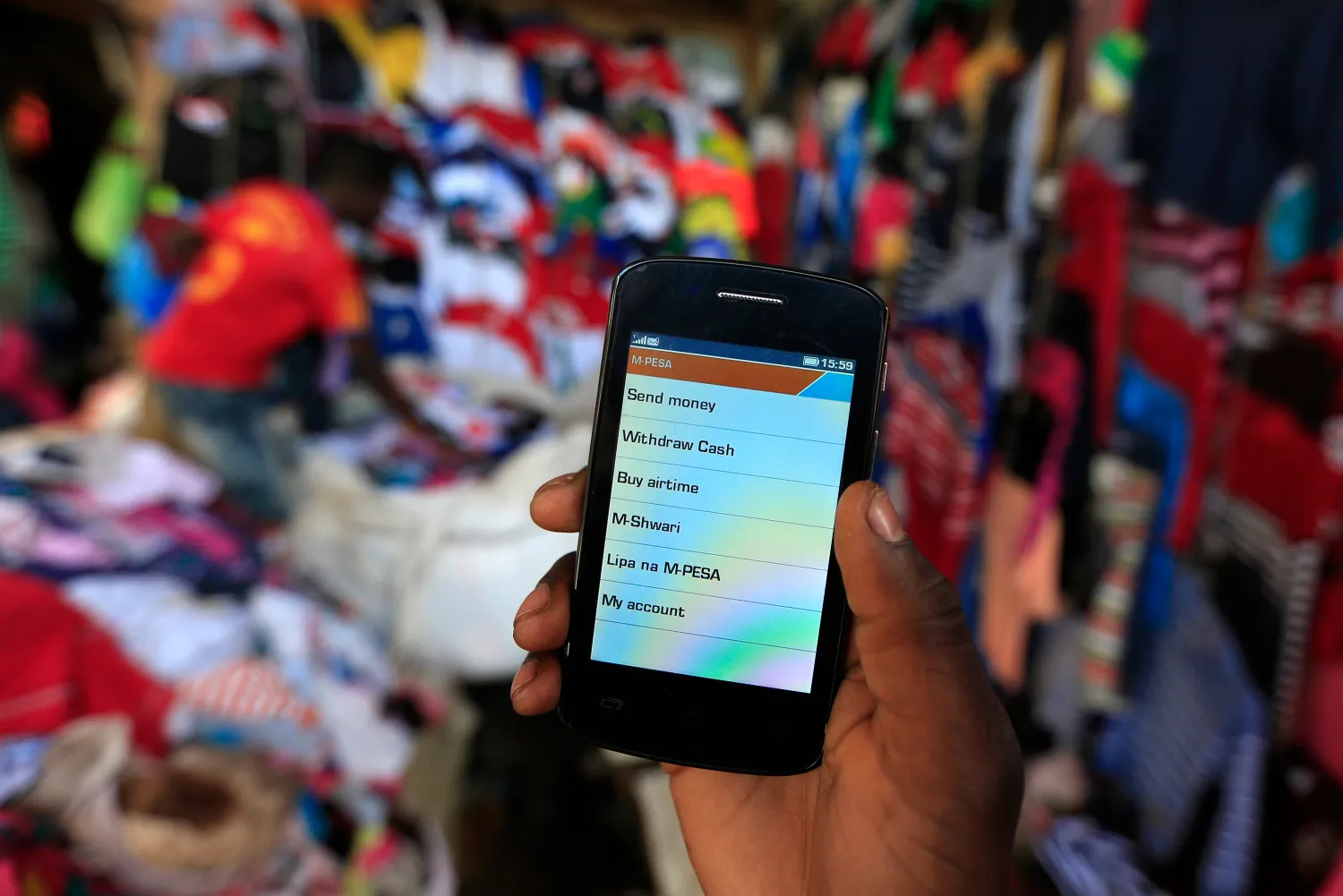

Fintech

Inside Rwanda’s Cloud Battle Against Big Tech

Structural Constraints

The continent faces a $130–$170 billion infrastructure financing gap annually. This shapes how startups build and scale.

A Rwanda startup challenges global cloud giants as Africa’s data demand surges and local infrastructure gaps widen.

👤 FROM CLASSROOM CODE TO CLOUD INFRASTRUCTURE

Stretch Cloud did not begin in a venture-backed lab or a global accelerator.

It emerged from the Rwanda Coding Academy — a government-backed institution designed to produce elite software engineers. From this environment, a team led by Jean-Luc Sauvé (widely referred to as Jeanluke) moved beyond coding applications and into building infrastructure.

According to Techinika coverage, the company launched with approximately 2 million Rwandan francs in initial capital — a modest entry point for a business operating in one of the most capital-intensive segments of technology.

Subsequent reporting linked to IGIHE coverage associates the startup with a valuation estimate of roughly $2.5 million, signaling early traction despite limited disclosed funding rounds.

This origin matters.

It reflects a shift in African tech: founders moving beyond software applications into the deeper, more complex layer of digital infrastructure.

📈 40% INTERNET PENETRATION DRIVES CLOUD DEMAND

The market Stretch Cloud is entering is expanding rapidly.

According to the International Telecommunication Union, internet penetration across Africa has surpassed 40%, with growth driven primarily by mobile connectivity.

At the same time, demand for digital services continues to accelerate:

- fintech platforms are scaling

- e-commerce ecosystems are expanding

- governments are digitizing services

According to the International Finance Corporation, Africa’s digital economy could reach $180 billion by 2025.

However, infrastructure has not kept pace with demand.

⚙️ LOCAL CLOUD VS GLOBAL SYSTEMS

Most African data still flows through infrastructure located outside the continent.

According to the World Bank digital development data, businesses in Africa face higher relative costs for cloud services due to offshore hosting, foreign currency pricing, and latency issues.

Stretch Cloud’s model directly responds to this gap.

According to Techinika, the platform emphasizes:

- localized hosting

- reduced latency

- compliance with regional requirements

- pricing adapted to local markets

This creates a different value proposition from global hyperscalers such as AWS or Microsoft Azure, which prioritize scale over regional customization.

💰 $130–$170 BILLION INFRASTRUCTURE GAP DEFINES THE MARKET

The deeper constraint is structural.

According to the African Development Bank, Africa faces an infrastructure financing gap of between $130 billion and $170 billion annually.

Cloud infrastructure sits within this broader deficit.

Unlike software startups, infrastructure companies require sustained capital investment in:

- servers

- data centers

- bandwidth capacity

- system redundancy

At the same time, funding conditions are tightening.

According to the World Bank, global financial tightening has reduced capital flows into emerging markets, limiting access to venture funding.

This creates a dual pressure:

- rising demand for infrastructure

- constrained capital to build it

🏦 CAPITAL CONSTRAINTS RESHAPE STARTUP STRATEGY

This environment is forcing a shift in how startups scale.

Instead of pursuing rapid expansion through external funding, companies like Stretch Cloud are building within constraints:

- focusing on local markets

- prioritizing cost efficiency

- scaling gradually

This approach reflects a broader trend across African tech, where founders are increasingly aligning growth strategies with capital realities rather than global venture models.

🧠 WHAT ENTREPRENEURS CAN LEARN

Stretch Cloud’s trajectory offers several clear lessons:

1. Build within structural gaps

The company targets a measurable infrastructure deficit rather than a speculative market.

2. Leverage talent ecosystems

Its roots in Rwanda Coding Academy highlight the role of technical training institutions in shaping startups.

3. Start with constrained capital

Launching with about 2 million RWF demonstrates disciplined early execution.

4. Align with macro trends

The model fits within rising digital demand and policy shifts toward data localization.

5. Compete through localization

Local pricing and infrastructure create differentiation against global players.

🔄 POWER SHIFT: FROM CLOUD USERS TO CLOUD BUILDERS

Africa’s cloud market is entering a new phase.

For years, the continent operated primarily as a user of global infrastructure. Data moved across borders, and businesses relied on systems built and controlled elsewhere.

That model is now under pressure.

According to the World Economic Forum, governments are placing increasing emphasis on data sovereignty, pushing for local storage and processing.

At the same time, demand for digital services continues to rise.

This combination is reshaping the competitive landscape.

Global providers still dominate scale and capital. But local players are beginning to compete on proximity, pricing, and regulatory alignment.

Stretch Cloud sits at this intersection.

📌 FINAL TAKE: THE INFRASTRUCTURE GENERATION

Jeanluke’s journey reflects a broader shift in African entrepreneurship.

Earlier waves built applications. The current wave is beginning to build infrastructure.

According to the International Finance Corporation, digital infrastructure will remain a core constraint — and opportunity — in Africa’s growth story.

Stretch Cloud is still early.

Its success will depend on execution, funding access, and its ability to scale against global competition.

But its emergence signals something larger:

a move toward locally built digital systems.

🧠 THE PARAGRAPH THAT STICKS

Africa is no longer just logging into the cloud — it is beginning to build it.

And if that shift continues, the question will not be whether global platforms serve African markets, but whether African infrastructure starts to define them.

Fintech

Uganda Cash Limits Accelerate Digital Shift

Interbank cheque thresholds have been cut by 50% across multiple currencies, further narrowing reliance on paper-based transactions. The change reinforces a broader retrenchment of traditional payment instruments.

Bank of Uganda imposes cash withdrawal caps and cheque cuts, accelerating Uganda’s shift toward digital payments and formal finance rails.

Uganda Rebuilds Its Payment Architecture

Uganda is entering a structural shift in how money moves through its economy. The Bank of Uganda has introduced system-wide limits on over-the-counter cash withdrawals and sharply reduced interbank cheque thresholds, effective 1 January 2027.

Importantly, this is not a routine banking adjustment. Instead, it reflects a deeper redesign of the country’s payment system.

In simple terms, Uganda is moving from cash tolerance to payment steering.

Cash Controls Introduce a New Liquidity Framework

The new rules create direct limits on how much cash can move through banking halls.

For individuals, daily withdrawals are capped at UGX 50 million ($13,245), while weekly limits are set at UGX 250 million ($66,225). At the same time, corporate accounts face higher thresholds of UGX 500 million ($132,450) per day and UGX 2.5 billion ($662,250) per week.

However, the structure is important. Electronic channels are fully exempt.

RTGS transfers, Electronic Funds Transfers (EFTs), and mobile money transactions remain unrestricted. As a result, the policy does not block liquidity. Instead, it redirects it.

Therefore, Uganda is not reducing money movement. It is reshaping how money moves.

Cheque System Is Being Phased Down

In parallel, Uganda has reduced interbank cheque thresholds by 50% across five currencies.

- UGX cheques fall from 10 million to 5 million

- USD cheques drop from $2,750 to $1,375

- EUR cheques fall from €2,250 to €1,125

- GBP cheques decline from £2,200 to £1,100

- KES cheques drop from KSh300,000 to KSh150,000

These changes apply only to interbank clearing.

However, the signal is broader. Cheques are being pushed into low-value use cases.

Therefore, Uganda’s payment system is steadily removing mid-tier paper instruments from active circulation.

In effect, three layers are emerging:

- digital rails (dominant)

- limited cash (controlled)

- shrinking cheques (secondary)

Digital Infrastructure Becomes the Core System

Uganda’s reforms build on already strong digital growth.

Electronic payments reached UGX 326.3 trillion ($86.4 billion) in 2025. In addition, transaction volumes rose more than 20%, reaching 8.4 billion transactions.

Meanwhile, mobile money adoption has reached scale. There are now 36.7 million active users supported by more than one million agents nationwide.

This matters for one key reason.

Digital payments are no longer emerging tools. Instead, they are already the dominant settlement layer in Uganda’s economy.

Therefore, the central bank’s policy does not introduce digital payments. It consolidates them.

Telecom Operators Gain Structural Advantage

As cash usage becomes constrained, mobile money operators are gaining structural importance.

Platforms operated by MTN Uganda and Airtel Uganda sit directly inside this transition.

In particular, high-volume cash users—such as traders, SMEs, and cross-border operators—are expected to shift toward mobile money rails.

As a result, telecom firms are no longer just service providers. They are becoming core financial infrastructure nodes.

This shift also changes competitive dynamics in Uganda’s financial system. Banks increasingly depend on telecom rails for retail transaction flow, while telecoms gain more control over payment liquidity.

Policy Design Shows a Behavioral Strategy

The structure of the reforms reveals a clear policy logic.

First, cash is limited. Second, digital systems are unrestricted. Third, cheques are compressed.

Taken together, this creates a directional system.

However, the goal is not prohibition. Instead, it is behavioral migration.

In other words, users are not forced out of cash. They are economically encouraged to move away from it.

This approach reflects a broader trend in emerging markets where regulators use system design—not bans—to shape financial behavior.

A Strategic Shift From Incentives to Enforcement

Uganda’s National E-Payments Strategy 2021–2026 focused on infrastructure building and voluntary adoption.

Now, the next phase is different.

The strategy is shifting from:

- building systems → enforcing usage

- promoting adoption → steering behavior

- optional digitalization → structural digital dominance

This transition is supported by scale data:

- UGX 326.3 trillion in digital transactions

- 8.4 billion transaction volumes

- 36.7 million mobile money users

Therefore, Uganda is moving past adoption stage and entering system consolidation stage.

Policy Friction: Pricing vs Adoption

However, a contradiction remains in the system.

While digital payments are being promoted structurally, transaction costs remain relatively high for low-income users.

A proposed reduction in mobile money excise duty from 0.5% to 0.25% was rejected in the 2026/27 budget cycle.

As a result, users face a dual pressure:

- higher friction in digital transactions

- tighter limits on cash usage

This creates a policy tension.

Therefore, adoption speed may depend not only on regulation, but also on affordability.

Informal Economy Remains the Key Constraint

Despite strong digital growth, cash remains deeply embedded in Uganda’s real economy.

Agriculture, artisanal mining, and informal trade continue to rely heavily on physical cash flows.

However, the central bank has introduced discretionary waivers for supervised financial institutions. These waivers are conditional and require enhanced due diligence.

This structure effectively creates a dual-track system:

- regulated digital economy

- monitored cash economy

Therefore, Uganda is not eliminating cash. It is reorganizing its role.

Regional Implications for East Africa

Uganda’s model is significant for regional policy design.

Across East Africa, most regulators have focused on incentives and infrastructure expansion. Uganda is now adding direct cash constraints to accelerate digital migration.

This makes the policy structurally different.

If successful, it could influence future frameworks in Kenya, Tanzania, and Rwanda, especially in areas such as:

- cash management policy

- digital tax enforcement

- payment system hierarchy design

Therefore, Uganda is effectively testing a new regulatory model for emerging-market payment systems.

Intelligence Takeaway

Uganda’s cash withdrawal limits and cheque reductions represent more than payment reform.

They signal a structural redesign of the financial system.

Instead of encouraging digital adoption through incentives alone, the country is now actively shaping transaction behavior through system constraints.

As a result, Uganda is entering a new phase where:

- cash is constrained

- digital rails are dominant

- cheques are marginal

Ultimately, the policy marks a shift from financial inclusion strategy to financial system engineering.

And in that shift, Uganda is positioning itself as one of the most intervention-driven digital payment environments in Africa’s current monetary evolution cycle.

Fintech

Black Swan Tanzania Bloomberg Startup List

Africa’s Fintech Ecosystem Is Reshaping

Black Swan operates within a broader shift toward data-driven financial infrastructure. This is redefining how credit markets function.

Black Swan is named in Bloomberg’s 2026 African startups list, highlighting Tanzania’s rise in AI-driven credit data innovation.

Tanzanian fintech Black Swan has been featured in Bloomberg’s “25 African Startups to Watch in 2026”, published on 28 May 2026, becoming the only startup from Tanzania included in the list.

The selection, compiled by Bloomberg Technology, highlights firms operating in environments where traditional systems have failed to deliver effective access to services such as credit, healthcare, logistics, and payments. The report notes that many of these startups are building solutions in markets where infrastructure gaps remain structurally entrenched.

(Source: Bloomberg Technology – African Startups to Watch 2026)

Importantly, Black Swan’s inclusion reflects a growing investor focus on data-led credit infrastructure models, rather than traditional consumer fintech applications.

🟩 Core Business Model: How Black Swan Works

Black Swan operates in the alternative credit intelligence segment, using non-traditional data sources to assess borrower risk.

Instead of relying on formal credit histories, the company evaluates:

- utility bill payments

- mobile money transactions

- digital behavioural patterns

- informal income signals

This allows lenders to extend credit to individuals and small businesses that are typically excluded from formal banking systems.

In effect, Black Swan is building a data-driven credit scoring layer for underbanked markets.

🟨 “Fingers”: Structural Market Data

According to the World Bank Global Findex, a significant portion of adults in emerging markets remain outside formal credit systems due to lack of documentation or banking history.

At the same time:

- informal economies account for a large share of employment in Sub-Saharan Africa

- traditional credit bureau coverage remains uneven across markets

- fintech adoption continues to rise through mobile money ecosystems

These structural gaps create the conditions for alternative credit models to scale.

🟥 Ecosystem Context: Where Black Swan Fits

Black Swan operates within a layered financial ecosystem:

1. Credit Infrastructure Layer

- weak traditional credit bureau penetration

- collateral-heavy lending models

2. Digital Financial Layer

- mobile money systems

- fintech payment platforms

- digital transaction rails

3. Lending Institutions

- commercial banks

- microfinance institutions

- digital lenders

4. Regulatory Environment

- central bank oversight

- data protection rules

- credit reporting frameworks

Within this structure, Black Swan acts as a data intelligence layer, enabling lenders to price risk more accurately.

🟦 Tecno Layer: How the System Works

Black Swan’s model functions through three core processes:

1. Data Aggregation

It collects non-traditional financial signals such as utility payments and transaction activity.

2. Risk Modelling

Machine learning systems translate behavioural data into creditworthiness indicators.

3. Credit Intelligence Output

The insights are sold to lenders, enabling them to approve or reject loans more accurately.

The business model is therefore based on credit scoring-as-a-service, rather than direct lending.

🟨 Investor Interpretation

From an investor’s perspective, Black Swan sits within a fast-growing segment of alternative credit infrastructure providers.

This category is increasingly attractive because it:

- expands addressable lending markets

- reduces dependency on collateral-based systems

- improves underwriting efficiency

- integrates informal economies into formal finance

However, risks remain, particularly around:

- data privacy regulation

- model accuracy in fragmented markets

- scalability across different countries

Therefore, the investment case is best understood as early-stage infrastructure building, rather than mature fintech scaling.

🟥 Strategic Signal

Black Swan’s inclusion in Bloomberg’s list is not simply symbolic.

Instead, it reflects a broader structural shift in African fintech:

from payments-driven innovation

to data-driven credit infrastructure systems

This shift suggests that the next phase of fintech growth in Africa will be driven less by consumer apps, and more by backend financial intelligence systems.

Fintech

NALA Raises US$50M for Payment Rails Growth

Stablecoins Improve Cross-Border Payments

Stablecoin-linked systems are helping reduce cost and delay in international transfers. As a result, money movement across borders is becoming more efficient.

Tanzania’s NALA secures up to US$50M MUFG-backed facility to scale stablecoin payment infrastructure across global corridors.

🟦 NALA’s US$50M Facility Signals New Phase in Global Payments

Intelligence Brief | Fintech & Cross-Border Money Flow

Tanzanian fintech NALA has secured a major funding package that highlights a clear shift in how global investors view African fintech firms. Importantly, the company is now being seen less as a consumer app and more as a payment systems builder.

On 28 May 2026, NALA announced it had secured a US$25 million credit facility, which can rise to US$50 million, from Liquidity, a platform backed by Japan’s MUFG through Mars Growth Capital.

The deal was reported by Launch Base Africa.

At the same time, the structure of the deal shows a wider trend. Investors are now supporting debt-based growth funding instead of equity dilution, especially in fintech infrastructure businesses.

🟩 Why This Deal Matters

This financing is important for three simple reasons.

First, it provides growth capital without diluting shareholders. Therefore, NALA can expand without giving up ownership.

Second, it supports stablecoin-linked payment corridors. As a result, the company can move money faster across borders.

Third, it signals rising trust in African payment infrastructure.

Importantly, the financing was arranged through Mars Growth Capital, which is backed by Japanese banking group MUFG.

🟨 NALA’s Own Position: From Product to System

NALA has also clearly shifted how it describes its business.

According to its statement reported by Launch Base Africa, the company said the facility will support:

“reliable and scalable payment infrastructure across international remittance corridors.”

This statement is key.

It shows that NALA is no longer focusing only on remittances. Instead, it is focusing on building systems that move money across countries.

In simple terms, the company is moving from a product model to a network model.

🟥 Stablecoins and Faster Money Movement

At the same time, the deal highlights the growing use of stablecoins in global payments.

Traditionally, sending money across borders has been slow and expensive. However, many transactions still rely on old banking systems.

According to the World Bank Remittance Prices database, Sub-Saharan Africa remains one of the most expensive regions for sending money.

Therefore, new systems are being built to reduce cost and time.

Stablecoin-based systems help by:

- reducing currency conversion steps

- lowering transfer delays

- improving liquidity flow

- simplifying settlement

As a result, companies like NALA are trying to make cross-border payments faster and cheaper.

🟦 Shift in Investor Thinking

From an investor view, this deal also shows a change in thinking.

In the past, fintech companies were valued based on user growth. However, this is changing.

Now, investors are focusing more on:

- transaction systems

- payment networks

- infrastructure revenue

- long-term cash flow stability

This is important because infrastructure businesses tend to generate more stable income over time.

In addition, they are harder to replace once they are built into payment systems.

Therefore, NALA’s valuation story is shifting from growth app to payment infrastructure platform.

🟨 Africa’s Role in Global Payments

At the same time, Africa is becoming more important in global money flows.

This is happening for three main reasons.

First, remittances into Africa are large and growing.

Second, mobile money systems are widely used across the continent.

Third, cross-border trade is increasing under AfCFTA.

Because of this, payment systems in Africa are becoming part of global financial infrastructure.

Therefore, companies like NALA are no longer local players. Instead, they are becoming part of global payment networks.

🟥 Risks Still Remain

However, risks still exist.

Regulation is not fully clear for stablecoins. In addition, different countries apply different rules.

There are also concerns about:

- compliance requirements

- currency controls

- anti-money laundering systems

- cross-border oversight

As a result, growth will depend on how well companies adapt to regulation.

🟦 Market View: A Clear Direction Shift

Overall, this deal does not just show funding activity. Instead, it shows a clear direction shift in fintech.

Importantly, three changes are now visible:

First, African fintech firms are moving into infrastructure roles.

Second, global banks are funding payment rails instead of apps.

Third, stablecoins are entering mainstream payment systems.

Therefore, the industry is moving toward a new structure.

🟩 Conclusion: From App to Payment Rail

NALA’s US$50 million expandable facility marks an important step in this transition.

The company is no longer being viewed only as a remittance platform. Instead, it is being positioned as part of the infrastructure that moves money globally.

In conclusion, this deal shows a wider truth.

The future of fintech is not only about apps. It is about the systems that connect global payments.

Fintech

Rwanda Builds $5B Cross-Border Finance Rail

Cross-border settlement systems are becoming the next competitive frontier in East African finance. Rwanda is using APIs and mobile money integration to strengthen regional transaction flows.

Rwanda accelerates a $5B cross-border finance rail linking East Africa through banking APIs, fintech integration, and digital payments.

Rwanda Builds $5B Cross-Border Finance Rail

Rwanda is accelerating an ambitious financial infrastructure strategy that could reshape how money moves across East Africa.

Rather than focusing on traditional banking expansion alone, Kigali is positioning itself as a regional interoperability hub where cross-border liquidity can move faster through integrated payment systems.

The strategy aligns with broader digital finance priorities promoted by the World Bank Digital Development program, which has repeatedly identified fragmented payment infrastructure as a major obstacle to trade integration in emerging markets.

Kigali Pushes Financial Infrastructure Integration

The real significance of Rwanda’s strategy lies in the infrastructure layer rather than retail banking growth.

Instead of relying on branch expansion, Rwanda is building interoperability systems that allow:

- banks to connect directly with fintech platforms

- mobile money operators to integrate with settlement systems

- cross-border transactions to move more efficiently across East African corridors

Consequently, Rwanda is beginning to emerge as a regional transaction-routing centre despite its relatively small domestic market.

The National Bank of Rwanda has consistently prioritised financial digitisation and interoperability as part of the country’s long-term economic modernisation agenda — see the National Bank of Rwanda.

At the same time, institutions such as the Kigali International Financial Centre are actively positioning Rwanda as a gateway for regional investment flows and financial services expansion.

Banks Are Becoming Infrastructure Platforms

Commercial banks in East Africa are no longer operating solely as deposit-taking institutions.

Instead, they are transforming into infrastructure platforms that connect payment systems, fintech applications, and mobile transaction ecosystems.

For example, Bank of Kigali has increasingly expanded digital banking integration and API-enabled financial services designed to support interoperability across multiple payment channels.

Similarly, telecom-driven payment systems are becoming central to everyday commerce. Mobile money platforms linked to MTN and Airtel ecosystems already process large transaction volumes across East Africa, particularly in retail trade and SME payments.

As a result, the distinction between banks, fintech firms, and telecom operators is gradually narrowing.

This structural convergence matters because the future of African finance is increasingly being shaped by transaction infrastructure rather than physical banking networks.

The Real “Fingers” Behind the System

Several institutional “fingers” are quietly shaping the emerging financial rail across East Africa.

Regulators

- National Bank of Rwanda

- Central Bank of Kenya

- Bank of Uganda

These regulators are increasingly coordinating around interoperability frameworks and regional payment standards.

Banking institutions

- Bank of Kigali

- Equity Group subsidiaries

- KCB Group-linked operations

- regional commercial banks integrating API systems

Telecom and mobile money operators

- MTN Mobile Money

- Airtel Money

These firms now function as transaction infrastructure providers rather than simple telecom operators.

Development finance institutions

Organisations such as the International Finance Corporation and the Trade and Development Bank continue to support financial integration projects across the region.

Consequently, the financial rail is becoming a hybrid system combining public regulation, private banking infrastructure, and telecom-led transaction networks.

Why the $5 Billion Figure Matters

The estimated $5 billion figure linked to the emerging rail reflects projected annual transaction throughput across interconnected systems.

Importantly, the figure does not represent direct infrastructure spending. Instead, it refers to the volume of financial flows expected to move through interoperable regional payment channels.

Those flows include:

- SME trade payments

- cross-border mobile money settlements

- regional business transactions

- supplier and logistics payments

- digital banking transfers

Therefore, the real competition is no longer about opening more branches.

Instead, financial institutions are competing to control:

- transaction routing

- settlement infrastructure

- interoperability standards

- API connectivity

- payment processing ecosystems

This shift mirrors broader global trends where digital payment systems increasingly determine financial influence.

East Africa’s Payments War Is Intensifying

Competition across East Africa’s financial system is entering a new phase.

Previously, banks focused heavily on deposits and branch expansion. Today, however, the battle revolves around who controls transaction ecosystems and settlement infrastructure.

Rwanda’s strategy is particularly notable because it emphasises neutrality and connectivity rather than domestic scale alone.

Consequently, Kigali is becoming attractive to:

- fintech startups

- regional banks

- digital payment firms

- cross-border investors

At the same time, East African governments are pushing stronger regional trade integration, increasing demand for efficient settlement systems capable of handling multi-country transactions.

The African Continental Free Trade Area (AfCFTA) framework has further intensified pressure for interoperable payment systems that can reduce transaction costs across African economies — see the AfCFTA Secretariat.

Investors Are Watching the Infrastructure Layer

Global investors are increasingly treating digital payments infrastructure as a long-term strategic asset class across Africa.

Importantly, Rwanda offers several characteristics that investors typically favour:

- regulatory consistency

- strong digital governance

- coordinated financial policy

- relatively stable macroeconomic management

Moreover, the country’s leadership has consistently promoted technology-driven economic modernisation as part of Rwanda’s broader transformation agenda.

This creates an environment where fintech firms, banks, and development finance institutions can test interoperable financial systems at regional scale.

Bottom Line

Rwanda is no longer simply building a domestic fintech ecosystem.

Instead, the country is constructing a regional cross-border finance rail designed to integrate banking APIs, mobile money infrastructure, and digital settlement systems across East Africa.

Banks are becoming infrastructure platforms, telecom operators are evolving into financial transaction networks, and regulators are increasingly coordinating interoperability standards across borders.

As a result, Rwanda is positioning itself not merely as a fintech market — but as a strategic financial routing hub inside East Africa’s rapidly digitising economy.

Fintech

DRC Fintech Boom Reshapes Mobile Money Power

Banks and telecom operators are converging into hybrid financial systems, reshaping how money moves in the DRC economy.

DRC fintech expansion accelerates as mobile money, banks, and telecoms reshape Africa’s largest underbanked cash economy.

DRC Fintech Expansion Turns Mobile Money Into Core Financial Infrastructure

The Democratic Republic of Congo is no longer in a “future fintech market” phase — it is already operating a live, mobile-first financial system layered on top of a cash-dominant economy.

According to the World Bank, financial inclusion in low-income and fragile economies depends heavily on digital payment systems that can operate outside traditional banking networks. This is especially true in markets where physical banking infrastructure cannot scale quickly enough to meet population demand — see the World Bank Financial Inclusion Framework.

In the DRC, this framework is not theoretical — it is operational.

CASH ECONOMY STILL DOMINATES, BUT STRUCTURE IS SHIFTING

Despite rapid digital expansion, the DRC remains heavily cash-driven.

Development finance assessments consistently show that a large majority of daily transactions still occur outside formal banking channels, particularly in retail trade, transport, and informal commerce.

However, the shift underway is not about replacing cash entirely — it is about digitizing transaction layers above cash circulation.

This creates a hybrid structure:

- cash remains dominant at retail level

- mobile money dominates transfers and remittances

- banks dominate credit and structured finance

The International Finance Corporation (IFC) has repeatedly noted that mobile financial services are essential in markets where traditional banking cannot scale efficiently, particularly in Sub-Saharan Africa — see the IFC Financial Institutions Strategy.

THE CORE “FINGERS” CONTROLLING DRC FINTECH FLOWS

The DRC fintech ecosystem is highly concentrated around a small number of infrastructure controllers (“fingers”) that determine liquidity flow and transaction rails:

1. Vodacom Congo (M-Pesa ecosystem)

Vodacom operates one of the most widely used mobile money systems in the country, functioning as a de facto retail banking layer for millions of users.

2. Airtel Africa (Airtel Money)

Airtel Money plays a parallel role in payments, remittances, and agent-based cash networks, particularly strong in semi-urban corridors.

3. Orange DRC (Orange Money)

Orange Money maintains strong penetration in urban markets and cross-border Francophone payment corridors.

4. Central Bank of Congo (BCC)

The regulator is increasingly central to system stability, overseeing:

- payment system regulation

- monetary flow oversight

- financial compliance frameworks

Official communications from the Central Bank of Congo highlight ongoing modernization of payment infrastructure and digital financial system supervision — see the BCC official framework.

TELECOMS ARE FUNCTIONING AS BANKS

One of the most important structural shifts in the DRC is that telecom operators are no longer communication providers — they are financial infrastructure institutions.

Vodacom, Airtel, and Orange now control:

- mobile wallets (deposit substitutes)

- payment rails (transaction infrastructure)

- agent cash networks (physical liquidity layer)

- merchant payment systems

This mirrors a broader African pattern where telecom-led financial ecosystems substitute for underdeveloped banking networks.

The World Bank has previously emphasized that mobile money systems expand financial access in environments where traditional banking penetration is structurally limited — see the World Bank Digital Development Program.

BANKING SYSTEM IS ADAPTING, NOT COMPETING

Unlike mature financial markets where banks dominate fintech evolution, in the DRC banks are adapting to telecom-led infrastructure.

Rawbank — the country’s largest commercial bank — is increasingly integrating mobile money rails into its operations to expand credit access and deposit mobilization.

Rather than competing with telecom platforms, banks are becoming embedded financial layers within mobile ecosystems.

This creates a three-tier system:

- telecoms control transaction infrastructure

- banks control credit allocation

- mobile money acts as the interface layer

DEVELOPMENT FINANCE ACTORS ARE SYSTEM ANCHORS

A critical but underreported driver of the DRC fintech ecosystem is development finance capital.

Key institutional actors include:

- International Finance Corporation (IFC)

- World Bank Group

- British International Investment (UK)

- Proparco (France)

These institutions provide risk-sharing mechanisms, SME financing, and digital infrastructure funding that allow private operators to expand into high-risk markets.

Their role is not peripheral — it is structural, acting as stability anchors for financial system expansion.

WHY GLOBAL INVESTORS ARE WATCHING THE DRC

The DRC is attracting growing attention from fintech and emerging market investors for three structural reasons:

1. Scale opportunity

A population exceeding 100 million creates one of Africa’s largest untapped financial markets.

2. Extreme underbanking

Large portions of the population remain outside formal financial systems.

3. Mobile-first leapfrogging

The country is bypassing traditional banking expansion and moving directly into mobile-led finance.

This creates a high-growth, high-risk frontier fintech environment.

SYSTEM STRUCTURE: HYBRID FINANCIAL ARCHITECTURE

The DRC is not transitioning from cash to digital finance in a linear way.

Instead, it is building a multi-layer financial architecture:

- cash economy (dominant retail layer)

- mobile money (transaction layer)

- banking system (credit layer)

- development finance (stability layer)

This layered structure defines the current and future trajectory of the country’s financial system.

BOTTOM LINE

The Democratic Republic of Congo is undergoing a structural financial transformation driven by mobile money expansion, telecom-led banking infrastructure, and development finance intervention.

It is not simply a fintech growth story — it is the construction of a new financial operating system inside one of Africa’s largest underbanked economies.

Mobile money platforms are becoming the dominant transaction layer, telecom operators are acting as financial institutions, and banks are embedding themselves into digital ecosystems rather than competing with them.

The result is a hybrid financial system that is redefining how money moves across Central Africa.

Fintech

East Africa Digital Trade Boom: E-Commerce Shift

Logistics remains a key challenge for e-commerce growth. Companies are investing in delivery networks.

E-commerce and mobile payments are transforming East Africa’s trade, integrating logistics, finance, and cross-border digital markets.

💻 Digital Trade Boom: How E-Commerce Is Rewiring East Africa’s Economy

A structural transformation is unfolding across East Africa’s economy. It is not driven by heavy industry or infrastructure alone. Instead, it is powered by something less visible but equally powerful:

👉 The integration of digital platforms, payments, and logistics into a unified trade system.

E-commerce, once considered peripheral, is now reshaping how goods move, how businesses operate, and how consumers transact.

According to the World Bank and the International Telecommunication Union, digital adoption across Africa is accelerating, creating new pathways for trade and financial inclusion.

1. E-Commerce Moves From Niche to Mainstream

E-commerce in East Africa has shifted from a niche service to a core component of the economy.

Growth is driven by:

- Rising smartphone penetration

- Expansion of mobile internet access

- Changing consumer behaviour

- Increased trust in digital platforms

As a result, businesses are increasingly moving online.

The World Bank notes that digital commerce can significantly lower barriers to entry for small and medium-sized enterprises.

Therefore, e-commerce is becoming a market access tool.

2. Mobile Money Powers Digital Transactions

At the centre of this transformation is mobile money.

Platforms such as those operated by Safaricom have created a financial layer that supports digital trade.

Mobile money enables:

- Instant payments

- Low-cost transactions

- Financial inclusion for unbanked populations

According to the GSMA, Sub-Saharan Africa leads the world in mobile money adoption.

As a result, East Africa has developed one of the most advanced digital payment ecosystems among emerging markets.

3. Logistics Integration: The Missing Link

E-commerce cannot function without logistics.

Companies are investing heavily in:

- Last-mile delivery networks

- Warehousing systems

- Distribution hubs

However, logistics remains one of the biggest constraints.

Challenges include:

- Poor road infrastructure in some regions

- High delivery costs

- Fragmented supply chains

The African Development Bank highlights logistics as a key barrier to trade efficiency in Africa.

Therefore, integrating logistics with digital platforms is critical for scaling e-commerce.

4. Informal to Formal: A Structural Shift

Digital trade is gradually formalising parts of the informal economy.

Small businesses that previously operated offline can now:

- Reach wider markets

- Accept digital payments

- Build transaction histories

This transition has significant implications.

It:

- Expands the tax base

- Improves financial inclusion

- Enhances economic visibility

The World Bank notes that digital systems can help bring informal businesses into formal economic frameworks.

5. Cross-Border Digital Trade Expands

Digital platforms are also enabling cross-border trade.

Businesses can now:

- Sell products across national boundaries

- Access regional customer bases

- Use mobile payments for transactions

This aligns with broader regional integration efforts.

The United Nations Conference on Trade and Development highlights that digital trade is becoming a key driver of intra-African commerce.

Therefore, e-commerce is not limited to domestic markets—it is regional by design.

6. Platform Competition Intensifies

The digital trade space is becoming increasingly competitive.

Players include:

- E-commerce platforms

- Telecom companies

- Fintech firms

Each competes to control:

- Customer relationships

- Payment systems

- Data flows

As a result, the market is evolving into a platform-based economy.

Companies that control platforms gain significant market power.

7. Data as the New Trade Asset

Digital trade generates vast amounts of data.

Companies analyse:

- Consumer preferences

- Purchase behaviour

- Payment patterns

This data is used to:

- Improve services

- Target customers

- Develop financial products

The International Telecommunication Union notes that data is becoming a critical economic resource in digital economies.

Therefore, control of data equals control of value creation.

8. Investment Flows Into Digital Trade

Investors are increasingly targeting the digital economy.

Capital flows into:

- E-commerce platforms

- Fintech companies

- Logistics startups

These investments reflect confidence in long-term growth.

The World Bank highlights digital trade as a key driver of economic transformation in developing markets.

9. Regulatory Frameworks Are Catching Up

Governments are beginning to regulate digital trade more actively.

Focus areas include:

- Consumer protection

- Data privacy

- Digital taxation

- Payment system oversight

However, regulation remains uneven across countries.

Therefore, policymakers must balance innovation with control.

10. Conclusion: A New Trade Architecture

East Africa’s digital trade boom represents a fundamental shift.

Trade is no longer defined solely by physical movement of goods. Instead, it is shaped by:

- Digital platforms

- Payment systems

- Data flows

👉 In effect, e-commerce is creating a new economic architecture.

In conclusion, digital trade is not just transforming commerce—it is redefining how East Africa participates in the global economy.

-

Fintech3 weeks ago

Fintech3 weeks agoDRC Fintech Boom Reshapes Mobile Money Power

-

Banking & Finance4 weeks ago

Banking & Finance4 weeks agoKCB Q1 Profit Rises 15% as Assets Hit KSh2.25T ($17.3B)

-

Banking & Finance3 weeks ago

Banking & Finance3 weeks agoBK Group Profit Signals Rwanda’s Financial Hub Ambition

-

Telecommunications3 weeks ago

Telecommunications3 weeks agoSafaricom Ethiopia Challenges Ethio Telecom in Telecom Battle

-

Industries & Rankings3 weeks ago

Kenya Wins $324M from Diageo EABL Exit

-

Banking & Finance4 weeks ago

Banking & Finance4 weeks agoFamily Bank Profit Jumps 52% Ahead of NSE Debut

-

Fintech3 weeks ago

Fintech3 weeks agoBlack Swan Tanzania Bloomberg Startup List

-

Banking & Finance3 weeks ago

Banking & Finance3 weeks agoStandard Chartered AI Workforce Strategy Shift

-

Commercial Banking4 weeks ago

Commercial Banking4 weeks agoHF Group Rebrands to HFCB as Banking Transformation Accelerates

-

Banking & Finance4 weeks ago

Banking & Finance4 weeks agoEquity Group Q1 Profit Jumps 31% as Assets Hit KSh2 Trillion ($15.5bn)

-

Commercial Banking3 weeks ago

Commercial Banking3 weeks agoAbsa Kenya Earnings Hit by Rate Shift

-

DR Congo3 weeks ago

DR Congo3 weeks agoDRC SME financing expansion

-

Banking & Finance4 weeks ago

Banking & Finance4 weeks agoStanChart Kenya Profit Drops 26%

-

Banking & Finance3 weeks ago

Banking & Finance3 weeks agoEthiopia MFIs Post Record Profit Growth 2025

-

Boardroom Leadership3 weeks ago

Boardroom Leadership3 weeks agoCourt Shields Mbadi in Consolidated Bank Row

-

Boardroom Leadership3 weeks ago

Boardroom Leadership3 weeks agoStanChart Tanzania CEO Leadership Shift