Stanbic Holdings posts KSh13.71B ($100M) 2024 profit, up 12.8%, and raises dividends by 35% as it expands investment services and boosts market share in Kenya.

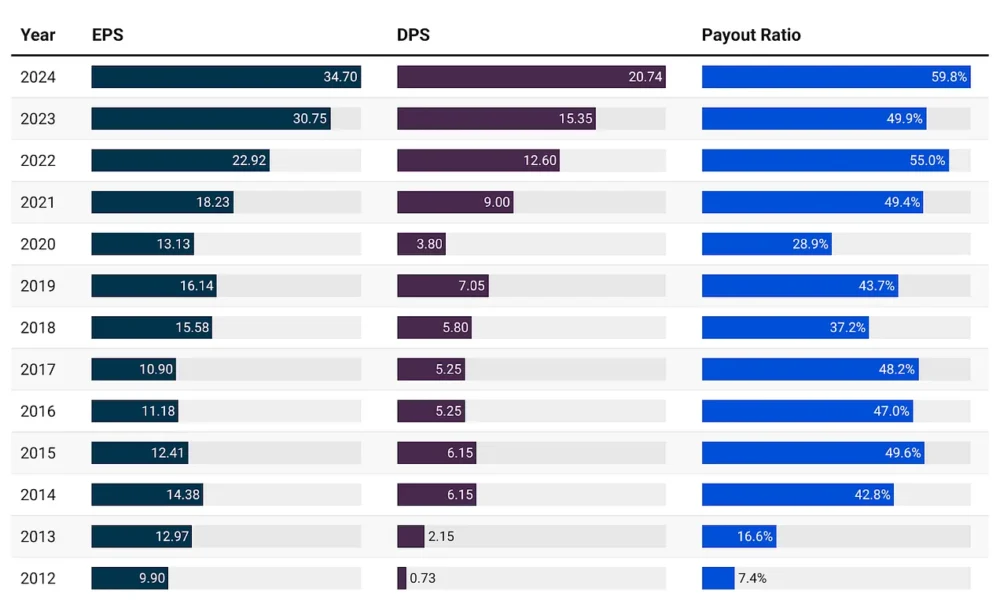

Stanbic Holdings Plc has posted a 12.8% rise in net profit to KSh13.71 billion (approx. $100 million) for the financial year ending December 31, 2024, up from KSh12.16 billion in 2023. The performance, released on March 5, 2025, demonstrates the bank’s resilience in a challenging macroeconomic environment across East Africa.

📌 Compare: Stanbic vs KCB Financial Performance in 2024

📌 See Also: Kenya’s Most Profitable Banks Ranked

💰 Dividend Payout Up 35% on Strong Earnings

Stanbic increased its total dividend to KSh20.74 per share ($0.15), up from KSh15.35 in 2023. This includes:

- KSh18.90 final dividend (pending approval)

- KSh1.84 interim dividend (paid September 2024)

The KSh8.1 billion ($59 million) payout equals 59.2% of net earnings, up from 49.9% the previous year—an indicator of growing shareholder confidence.

📌 Dividend Tracker: Kenya’s Top-Yielding Bank Stocks

📌 Guide: How to Invest in Stanbic on the NSE

📊 Subsidiary and Sector Performance

- Stanbic Bank Kenya delivered KSh13.5 billion ($98 million) in profit—18% growth YoY

- South Sudan operations: Profit fell 63% to KSh176 million ($1.3 million)

- SBG Securities: Profit plunged 87% to KSh20 million ($147,000) due to weak equities market

- Bancassurance unit: Net earnings declined 19% to KSh174 million ($1.3 million)

📌 SBG Securities: What Happened in 2024?

📌 East Africa’s Bank Insurance Models Explained

🏦 Asset Management and Market Expansion

In 2024, Stanbic launched a new asset management division, attracting KSh2.45 billion ($18 million) in assets within six months. This underscores growing demand for wealth management solutions across Kenya’s emerging investor base.

📌 Top Asset Management Firms in Kenya

📌 How Stanbic is Targeting Kenya’s Middle Class Investors

💹 Financial Highlights: NII Down, Provisions Drop

- Net Interest Income (NII): Fell 5.1% to KSh24.34 billion ($178 million)

- Interest Expenses: Surged to KSh21 billion ($154 million)

- Non-Interest Income: Slight decline to KSh15.4 billion ($113 million)

- Loan Loss Provisions: Halved to KSh3.09 billion ($22.6 million)

- Total Loans & Advances: Dropped 17.2% to KSh294.7 billion ($2.2 billion)

This reflects the combined effect of elevated borrowing costs, weak credit demand, and prudent risk mitigation.

📌 Understanding Net Interest Margins in Banking

📌 Why Loan Book Contraction Matters to Investors

🔮 CEO Outlook: Recovery in Sight for 2025

“While 2024 presented challenges, we are seeing positive signs that will drive lending growth in 2025, especially with interest rates expected to ease,”

— Joshua Oigara, CEO, Stanbic Bank Kenya and South Sudan

Stanbic is banking on interest rate normalization, digital innovation, and strategic partnerships to regain loan momentum and strengthen earnings.

📌 Oigara’s 2025 Strategy: From Lending to Innovation

🌍 Looking Ahead: Positioning for Growth

Stanbic Holdings’ 35% dividend increase reflects a solid capital base and a long-term value focus. With plans to grow its corporate lending, digital banking, and investment banking offerings, the group is positioning to take full advantage of:

- Kenya’s expected macroeconomic stabilization

- Rising demand for non-traditional banking services

- Pan-African capital market integration

📌 Stanbic Kenya: 2025 Investment Outlook

📌 Related: Kenya’s Top Banks Expanding Regionally

Leave a Reply