Banking & Finance

StanChart Kenya Profit Drops 26%

Asset quality improved significantly, with non-performing loans falling to their lowest level since 2015. The cleanup reflects a multi-year effort to reduce credit risk exposure after the post-pandemic stress cycle.

Standard Chartered Kenya’s Q1 2026 profit fell 26% as lower interest rates compressed margins despite strong loan growth and cleaner assets.]

🧠 Investor Intelligence Brief: Inside Standard Chartered Kenya’s Margin Compression Cycle

The first-quarter 2026 results from Standard Chartered Bank Kenya reveal one of the clearest signals yet that Kenya’s interest-rate easing cycle is beginning to materially compress banking-sector profitability — even among the country’s most conservatively managed Tier I lenders.

While several major Kenyan banks reported stronger earnings during the same period, largely supported by wider loan books and resilient fee income, Standard Chartered Kenya moved sharply in the opposite direction.

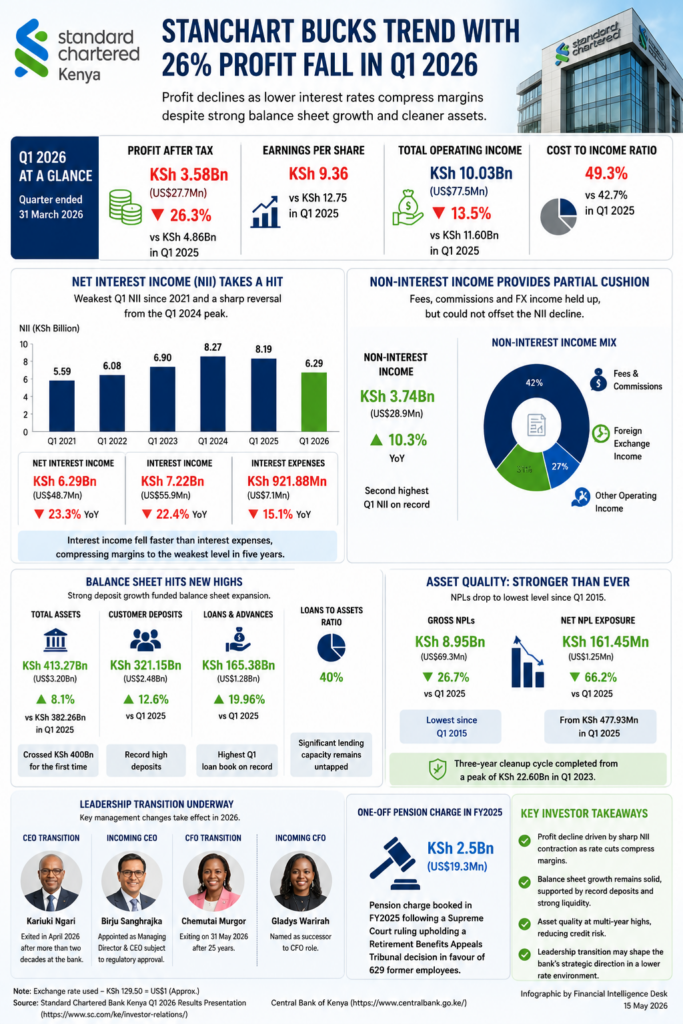

Profit after tax fell 26.3% to KSh3.58 billion (US$27.7 million) for the quarter ended March 2026, down from KSh4.86 billion (US$37.6 million) a year earlier.

The decline extends a difficult earnings cycle that had already seen the bank report a 38% fall in FY2025 profit following a one-off KSh2.59 billion (US$20 million) pension-related charge tied to a long-running legal dispute involving former employees.

👉 according to Standard Chartered Kenya investor disclosures

However, beneath the headline decline lies a more important institutional story: Standard Chartered Kenya is now confronting the structural limits of a liquidity-heavy, low-risk banking model during a falling-rate environment.

📉 THE REAL STORY: NET INTEREST INCOME COLLAPSE

The most consequential metric in the quarter was not profit.

It was the sharp deterioration in net interest income (NII), which fell 23.3% to KSh6.29 billion (US$48.7 million) — the weakest first-quarter NII performance since 2021.

This marks a dramatic reversal from the bank’s KSh8.27 billion (US$64 million) peak in Q1 2024.

Interest income declined 22.4% to KSh7.22 billion (US$55.9 million), while interest expenses fell at a slower pace of 15.1% to KSh921.88 million (US$7.1 million).

The implication is straightforward:

Standard Chartered’s asset yields are repricing downward faster than its funding costs.

That dynamic is increasingly important because the bank historically relied on:

- high-quality corporate lending,

- government securities,

- and liquidity management income

rather than aggressive balance-sheet expansion.

Now, as benchmark interest rates ease, the institution is finding it harder to preserve the exceptionally wide spreads that boosted profitability during the high-rate cycle of 2023–2024.

🏦 STANCHART IS BUCKING THE TIER I TREND

The contrast with Kenya’s other Tier I lenders is striking.

Banks such as Equity Group Holdings, KCB Group and Co-operative Bank of Kenya have generally managed to maintain stronger earnings momentum through:

- larger retail loan books,

- diversified regional operations,

- transaction banking scale,

- and broader non-funded income streams.

Standard Chartered Kenya, by contrast, remains structurally conservative.

That conservatism has historically protected asset quality and capital adequacy. However, it also limits upside during periods where peers aggressively expand lending volumes.

This divergence is now becoming more visible.

📊 BALANCE SHEET EXPANSION WITHOUT EARNINGS TRANSLATION

Ironically, the bank’s balance sheet continued expanding despite the earnings decline.

Total assets crossed the KSh400 billion (US$3.1 billion) threshold for the first time, reaching KSh413.27 billion (US$3.2 billion), up 8.1% year-on-year.

Customer deposits rose 12.6% to a record KSh321.15 billion (US$2.48 billion).

Meanwhile, loans and advances increased nearly 20% to KSh165.38 billion (US$1.28 billion) — the largest Q1 loan book in the bank’s history.

Yet this growth failed to translate into stronger profitability.

That disconnect matters because it suggests the institution is currently experiencing:

- margin compression,

- weaker asset repricing,

- and lower yield efficiency per unit of balance-sheet expansion.

In effect, Standard Chartered Kenya is growing larger while generating less incremental earnings from that growth.

🧭 ASSET QUALITY: THE STRONGEST AREA OF THE RESULTS

The strongest part of the quarter was unquestionably asset quality.

Gross non-performing loans (NPLs) declined 26.7% to KSh8.95 billion (US$69.3 million) — the lowest level since Q1 2015.

This completes a remarkable cleanup cycle from the KSh22.60 billion (US$175 million) peak recorded in Q1 2023.

Net NPL exposure narrowed even further to just KSh161.45 million (US$1.25 million).

For institutional investors, this is significant.

It confirms that the bank has largely succeeded in de-risking its balance sheet even as the broader Kenyan economy navigated inflation shocks, interest-rate volatility, and currency instability over the past three years.

However, cleaner assets alone cannot fully offset structurally weaker spreads.

📲 NON-INTEREST INCOME IS HOLDING — BUT NOT ENOUGH

Non-funded income provided partial relief.

Non-interest income rose 10.3% to KSh3.74 billion (US$28.9 million), supported by:

- foreign exchange trading,

- fees and commissions,

- and transaction-related income.

This was the second-highest Q1 non-interest income figure in the bank’s history.

Yet it still proved insufficient to offset the collapse in core lending margins.

That matters because Standard Chartered’s business model increasingly depends on:

- treasury services,

- corporate transaction flows,

- FX activity,

- and wealth-linked fee generation.

If rate compression persists into 2026–2027, the bank may need to accelerate growth in these non-funded businesses to stabilize returns.

🏛️ LEADERSHIP TRANSITION ADDS A SECOND LAYER OF UNCERTAINTY

The earnings slowdown is unfolding alongside major leadership changes.

Long-serving CEO Kariuki Ngari exited in April 2026 after more than two decades at the institution.

He is being succeeded by Birju Sanghrajka, subject to regulatory approval.

Separately, CFO Chemutai Murgor is set to leave after 25 years, with Gladys Warirah named as successor.

Leadership transitions during a margin compression cycle are rarely insignificant.

Investors will now watch whether the incoming management team:

- expands risk appetite,

- accelerates SME and commercial lending,

- or preserves the bank’s conservative operating philosophy.

⚠️ THE BIG INVESTOR QUESTION: CAN STANCHART ADAPT TO LOWER RATES?

The core investment question is no longer about asset quality.

It is whether Standard Chartered Kenya can adapt its earnings engine to a structurally lower-rate environment.

Its current model remains highly exposed to:

- interest margin sensitivity,

- treasury positioning,

- and premium corporate banking spreads.

That model worked exceptionally well during the high-yield environment of 2023–2024.

However, the current easing cycle is exposing the downside of conservative liquidity-heavy banking structures.

📌 INTELLIGENCE VERDICT

Standard Chartered Kenya remains one of the country’s strongest banks from a:

- capital,

- liquidity,

- and asset-quality perspective.

However, Q1 2026 suggests the bank is entering a more difficult strategic phase where:

- scale alone is insufficient,

- loan growth no longer guarantees profit growth,

- and earnings quality increasingly depends on fee income diversification.

The institution is not facing a solvency problem.

It is facing a profitability architecture problem.

That distinction matters — especially for global investors evaluating the sustainability of returns in African banking markets undergoing rapid monetary-policy transition.