Banking & Finance

Equity Group Q1 Profit Jumps 31% as Assets Hit KSh2 Trillion ($15.5bn)

Subsidiaries outside Kenya now contribute more than half of Equity Group’s profits, reflecting its accelerating regional diversification strategy. Markets such as the DRC and Tanzania are emerging as major growth engines for the bank.

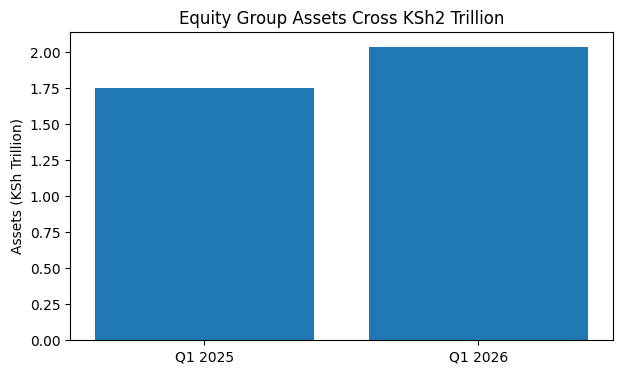

Equity Group Holdings posted a 31.3% jump in Q1 2026 profit before tax to KSh24.52 billion (US$190 million) as assets crossed KSh2 trillion (US$15.67 billion), driven by regional subsidiaries, digital banking growth and improving loan quality across East and Central Africa.

A Defining Moment for East Africa’s Banking Industry

The latest quarterly performance from Equity Group Holdings is not merely another earnings announcement. It represents a strategic turning point in the evolution of African banking, where regional expansion, digital finance and low-cost retail deposits are increasingly determining which institutions dominate the continent’s future financial architecture.

The Nairobi-based lender reported profit before tax of KSh24.52 billion (US$190 million) for the quarter ended March 31, 2026, marking a 31.3 percent increase compared to the same period last year.

Profit after tax climbed 24.1 percent to KSh19.05 billion (US$147 million), the highest first-quarter earnings in the group’s history.

Most significantly, total assets crossed the KSh2 trillion mark for the first time, reaching KSh2.036 trillion (US$15.67 billion), placing Equity among Africa’s fastest-growing banking groups outside South Africa and Nigeria.

According to the group, customer deposits rose 11.9 percent to KSh1.48 trillion (US$11.39 billion), while net loans increased 8.6 percent to KSh873.49 billion (US$6.73 billion).

James Mwangi’s Pan-African Banking Vision Gains Momentum

Group Managing Director and CEO James Mwangi says the lender is now positioning itself as a continental financial powerhouse rather than a Kenya-centric institution.

“The strength of our diversified business model and regional footprint continues to support sustainable growth while creating resilience across economic cycles,” Mwangi said during the release of the Q1 2026 financial results.

Mwangi added that the group, which currently serves 22.7 million customers across six African countries, intends to expand into 15 countries and reach 100 million customers by 2030 through acquisitions and organic growth.

The strategy increasingly mirrors the continental ambitions pursued by banking giants such as Ecobank Group and United Bank for Africa (UBA).

Regional Subsidiaries Now Drive the Group’s Growth Engine

For the first time in Equity’s history, subsidiaries outside Kenya contributed more than half of the group’s business.

Regional operations accounted for 52 percent of total assets and 51.7 percent of profit before tax, underscoring how the lender is reducing its reliance on the Kenyan economy.

This shift is strategically important as Kenya’s banking industry navigates slower private-sector credit growth, elevated public debt levels and persistent currency pressures.

Congo Emerges as Equity’s Most Strategic Foreign Market

The most consequential subsidiary remains Equity BCDC in the Democratic Republic of Congo (DRC).

The unit posted profit before tax of KSh7.2 billion (US$55.4 million), representing a 53 percent increase year-on-year.

Its assets rose to KSh760.6 billion (US$5.85 billion), while loans expanded 22 percent to KSh308.7 billion (US$2.38 billion).

The DRC operation is becoming strategically valuable not just because of retail banking growth, but because Congo sits at the centre of the global race for critical minerals including cobalt, lithium and copper — all essential for electric vehicles, battery storage systems and renewable energy infrastructure.

Banks with strong transactional networks in Congo are expected to play increasingly influential roles in trade finance, cross-border settlements and corporate banking linked to the global energy transition.

Tanzania Delivers the Fastest Growth Across the Group

Tanzania emerged as Equity’s fastest-growing subsidiary across virtually every performance metric.

Profit before tax surged 150 percent to KSh1.5 billion (US$11.6 million), while assets jumped 52 percent and loans expanded 68 percent.

The strong performance highlights how East Africa’s next banking battleground is shifting toward digital lending, SME financing and agency banking.

Rwanda also delivered strong momentum, with profit before tax rising 31 percent to KSh2.1 billion (US$16.2 million).

Uganda, however, was the only market to record weaker earnings, with profit after tax declining 20 percent to KSh0.8 billion (US$6.2 million), largely due to higher funding costs.

Falling Funding Costs Lift Profitability

One of the biggest drivers behind Equity’s strong earnings performance was a sharp reduction in funding costs.

The cost of deposits declined from 3.4 percent to 2.2 percent, enabling net interest income to rise 15.6 percent to KSh33.02 billion (US$255 million).

Meanwhile, interest expenses dropped 19.1 percent to KSh10.78 billion (US$83.2 million).

This trend is increasingly important across African banking markets where institutions capable of mobilising low-cost retail deposits are outperforming competitors reliant on expensive external borrowing.

Within Kenya, Equity Bank Kenya posted profit before tax of KSh11.9 billion (US$91.8 million), up 20 percent, while revenue climbed 14 percent to KSh27.2 billion (US$210 million).

Its net interest margin widened from 7.4 percent to 8.4 percent, while return on average equity improved to 28.9 percent.

Digital Banking Is Becoming Equity’s Core Competitive Weapon

Digital finance continues to reshape the group’s operational model.

According to the lender, 89.5 percent of all transactions are now processed digitally, compared to 74.9 percent in 2018.

Digital lending revenue rose 26 percent to KSh3 billion (US$23.1 million).

This reflects a broader structural shift taking place across African banking, where lenders are evolving into technology-driven financial ecosystems rather than traditional branch-led institutions.

The model has become increasingly attractive to investors seeking scalable financial platforms capable of reaching millions of previously unbanked consumers across Africa.

Insurance Expansion Adds a New Revenue Layer

Equity’s insurance business is also emerging as a meaningful contributor to profitability.

Its life, health and general insurance units posted combined gross written premiums of KSh4.46 billion (US$34.4 million), representing 30 percent growth.

Profit before tax rose 53 percent to KSh636 million (US$4.9 million).

Equity Life Assurance Kenya now has 21.3 million cumulative policies in force and controls 12.1 percent of Kenya’s Group Life and Credit Life insurance market.

Asset Quality Improves Despite Lingering Risks

Equity’s asset quality continued to improve despite persistent economic pressures across regional markets.

The group’s non-performing loan ratio declined to 10.6 percent from 14 percent a year earlier.

That compares favourably with Kenya’s banking industry average of 15.6 percent.

Loan loss provisions fell 16.9 percent to KSh2.8 billion (US$21.6 million), while IFRS coverage strengthened from 67 percent to 72 percent.

However, some pressure points remain.

The group’s cost-to-income ratio stood at 50.6 percent, above management’s target range of 46–49 percent, partly due to staff costs surging 34 percent to KSh11.7 billion (US$90.3 million) as the lender expanded hiring across regional subsidiaries.

Equity’s Transformation Reflects Africa’s Financial Future

Two decades ago, Equity was a struggling Kenyan building society.

Today, it has evolved into one of Africa’s most consistently compounding financial institutions.

From first-quarter profits of just KSh120 million (US$926,000) in 2006, the group now generates KSh19.05 billion (US$147 million) in quarterly profit after tax — roughly 159 times growth in two decades.

The broader significance of Equity’s rise lies in what it reveals about Africa’s economic future.

As the continent pushes toward deeper regional trade integration under the African Continental Free Trade Area (AfCFTA), banks capable of building cross-border financial infrastructure at scale are likely to emerge as some of the most strategically important institutions in Africa’s next growth cycle.

Equity appears determined to be one of them.