Commercial Banking

Co‑op Bank’s SACCO Funding Advantage Shines in 2025

While banks like KCB Group

reported larger absolute earnings, Co‑op Bank’s defensive funding mix through SACCOs gives it a competitive edge in cost of funds and asset quality.

Co‑op Bank Kenya leverages SACCO deposits for low‑cost funding, stable margins and record 2025 earnings, outperforming peers in resilience and profitability.

Co‑operative Bank’s SACCO Capital Engine: A Defensible Funding Model

In Kenya’s increasingly competitive banking sector, Co‑operative Bank of Kenya PLC (Co‑op Bank) has built a funding structure that stands apart. Rather than relying heavily on retail deposits or expensive wholesale funding — both of which can become volatile in unsettled markets — Co‑op Bank taps into the country’s extensive SACCO ecosystem for stable, low‑cost deposits that anchor its balance sheet.

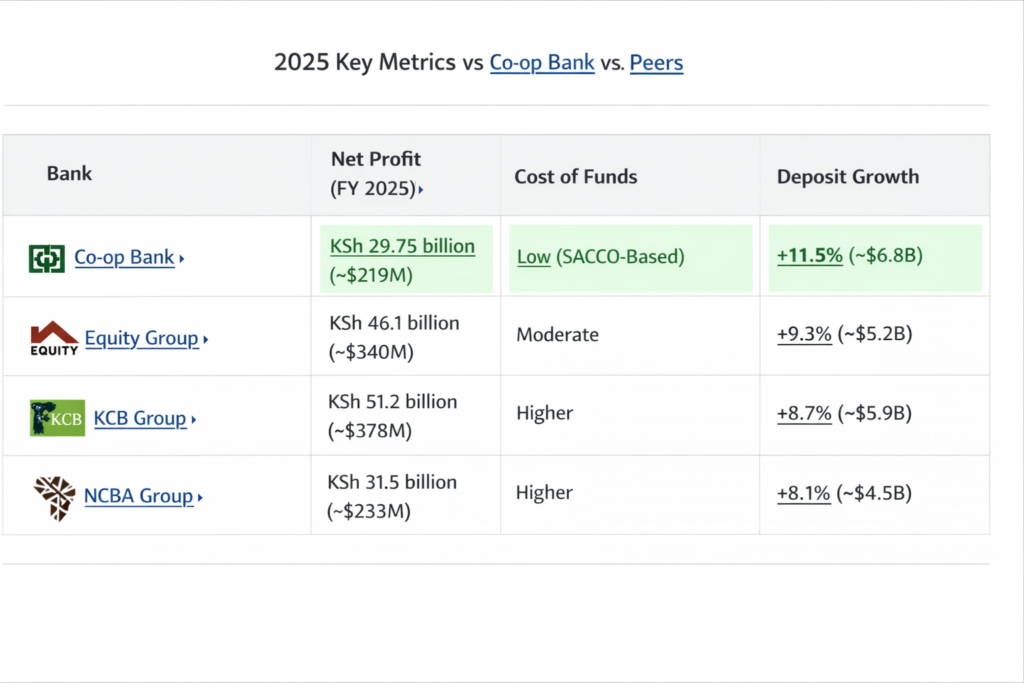

For the financial year ended December 31, 2025, the bank reported a record net profit after tax of KSh 29.75 billion (~$219 million), marking a 16.9 percent year‑on‑year rise from the prior year. This strong performance was paired with profit before tax of KSh 40.3 billion (~$296 million) — the highest in the bank’s history — reinforcing the resilience of its funding model.

At the same time, the board approved a 66.6 percent increase in the dividend to KSh 2.50 per share, equating to a record payout of KSh 14.6 billion (~$107 million). Such shareholder returns underscore not just profitability but confidence in the bank’s strategic direction and capital strength.

A Structural Cost Advantage

Funding costs are among the most critical drivers of net interest margins, which directly affect bank profitability. Traditional retail deposits — often used by banks such as Equity Group Holdings and KCB Group — tend to be more rate‑sensitive and expensive to retain, especially in tightening monetary environments. Co‑op Bank’s strategy, by contrast, leverages deposits mobilised through Savings and Credit Cooperative Organizations (SACCOs), which are typically:

- Sticky: driven by member contributions rather than opportunistic movements

- Lower‑cost: less driven by competitive interest rate bidding

- Predictable: based on systematic savings behaviors within cooperative communities

The result is a lower overall cost of funds than many of its peers — a structural moat that supports wider net interest margins even as competition for depositors intensifies.

Margin Stability in Volatile Markets

Kenya’s macroeconomic backdrop in recent years has been punctuated by interest rate fluctuations and cost pressures. During such cycles, banks dependent on rate‑sensitive funding often see their margins squeezed as they adjust deposit pricing to retain customers. Co‑op Bank’s SACCO‑anchored deposits behave differently; because they are driven by member savings patterns and community ties rather than purely yield chasing, they are inherently less volatile.

This stability has been pivotal to sustaining earnings quality. The bank’s combined focus on volume growth and cost discipline helped deliver record profit before tax of KSh 40.3 billion (~$296 million), even as peers faced margin pressure from higher funding costs and slower credit uptake.

Credit Quality and the SACCO Buffer

Another under‑recognised strength of Co‑op Bank’s model is its mitigation of credit risk. SACCO‑linked lending often incorporates group guarantees, mutual accountability frameworks, and historical contribution records for members — a quasi‑secured lending dynamic even in the absence of traditional collateral. This has helped the bank maintain comparatively lower non‑performing loan (NPL) ratios in segments influenced by SACCO activity.

The supportive cooperative ecosystem also plays a broader role beyond banking: according to the Cooperative Alliance of Kenya, SACCOs in the country mobilise over KSh 250 billion (~$1.8 billion) in savings and serve millions of members, offering a stable source of granular, community‑level capital.

Balancing Growth and Quality

Co‑op Bank’s approach contrasts with strategies pursued by some competitors, such as aggressive SME lending or rapid portfolio expansion. While banks like Equity and KCB continue to grow large SME portfolios and broader corporate lending books, Co‑op Bank appears to favour balance sheet quality and sustainability over sheer scale. That does not mean the bank ignores growth — far from it — but its emphasis remains on credit discipline, loan performance and manageable provisioning costs.

This approach bore fruit in 2025; deposit growth, net interest income expansion and disciplined cost management collectively drove the 16.9 percent rise in profit after tax to KSh 29.75 billion (~$219 million).

Liquidity Strength and Resilience

Liquidity risk is another dimension where Co‑op Bank’s SACCO‑anchored model shows strength. Institutions that depend heavily on wholesale funding or short‑term deposits often face abrupt funding cost spikes or rollover risks under stress scenarios. Co‑op Bank’s cooperative deposit base acts as a natural liquidity buffer, enabling the bank to maintain robust liquidity ratios without excessive reliance on market funding, even during tighter conditions.

This resilience is vital in a climate where banks sometimes face funding stress from rapid shifts in depositor behaviour, credit demand fluctuations, and macroeconomic uncertainties.

Competitive Landscape and Strategic Positioning

In the wider Kenyan banking landscape:

- KCB Group posted robust full‑year profits and proposed shareholder dividends, reflecting scale and diversified income streams.

- NCBA Group reported solid FY25 earnings with dividends rising 29 percent, signalling strong performance ahead of strategic shifts.

- Others like I&M Group and Family Bank delivered respectable profits and efficiency improvements, underscoring sector‑wide resilience.

Within this competitive set, Co‑op Bank’s defensive, SACCO‑anchored model provides a differentiated funding advantage — prioritising stability and consistent returns rather than purely top‑line growth.

Investor Takeaways: Predictability in a Shifting Market

For investors and market observers, Co‑op Bank’s 2025 performance highlights the value of predictability and structural funding resilience. Its SACCO‑driven deposit base not only supports earnings stability but also delivers meaningful returns to shareholders, as evidenced by the record dividend of KSh 14.6 billion (~$107 million).

In an environment where macroeconomic and competitive pressures are constant, Co‑op Bank’s model appears fine‑tuned for long‑term sustainability — a quiet, yet defensible engine of profitability rooted in cooperative capital and disciplined execution